Published on October 15, 2025

Understanding Personal Loans: A Complete Guide to Smart Borrowing

Personal loans can be powerful financial tools when used wisely. This comprehensive guide explains everything you need to know about how personal loans work, when they make sense, and how to avoid common pitfalls that could cost you thousands.

In today's financial landscape, personal loans have become increasingly accessible to consumers seeking funds for everything from debt consolidation to home improvements. Unlike mortgages or auto loans that are secured by specific assets, personal loans are typically unsecured, meaning they don't require collateral. This flexibility makes them attractive, but it also comes with important considerations that every borrower should understand before signing on the dotted line.

Whether you're considering a personal loan for the first time or looking to refinance existing debt, understanding the mechanics of personal lending, the true cost of borrowing, and the factors that influence your loan terms is essential for making informed financial decisions. This guide will walk you through everything from basic definitions to advanced strategies for evaluating loan offers and protecting your financial health.

What Are Personal Loans and How Do They Work?

A personal loan is a lump sum of money borrowed from a bank, credit union, or online lender that you repay in fixed monthly installments over a predetermined period, typically ranging from two to seven years. Unlike credit cards with revolving credit limits, personal loans provide a one-time disbursement with a structured repayment schedule that includes both principal and interest.

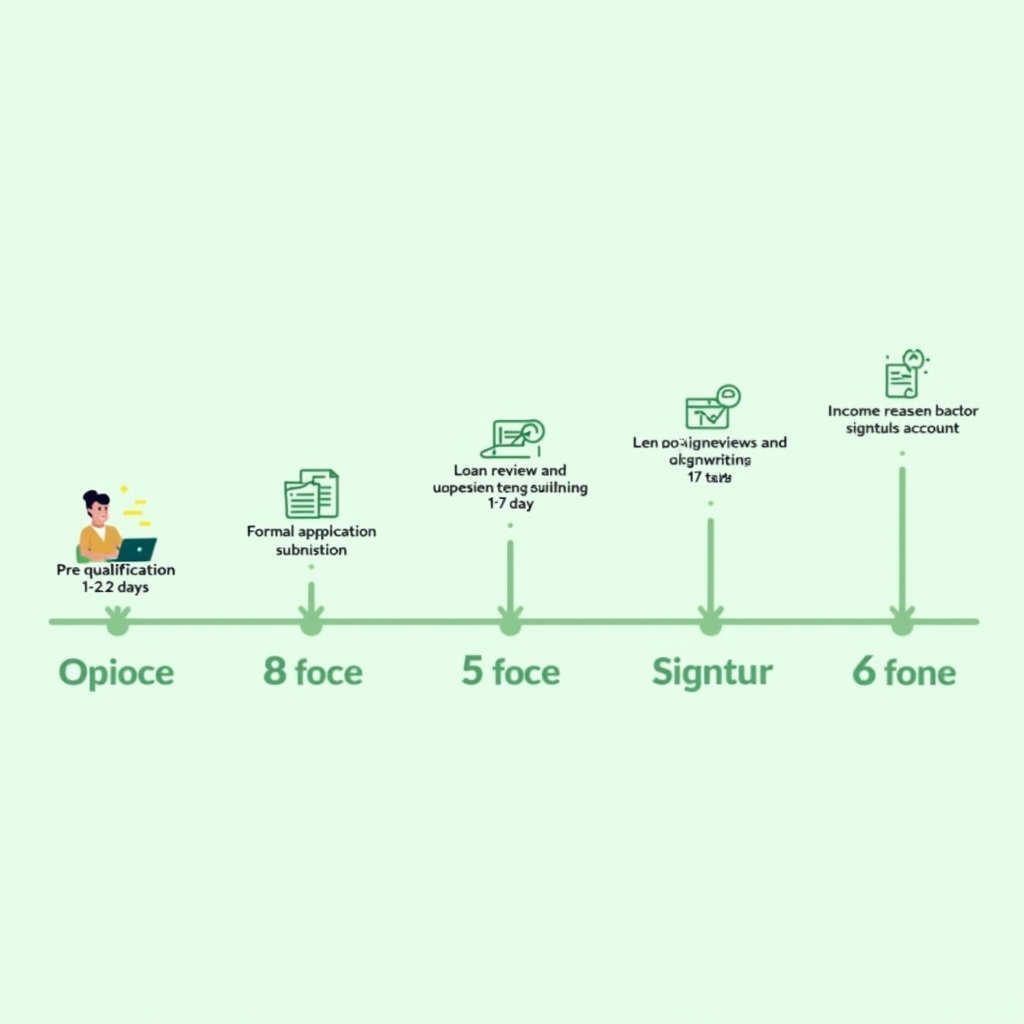

The loan process begins with an application where lenders evaluate your creditworthiness based on factors including your credit score, income, employment history, and existing debt obligations. Once approved, you'll receive the full loan amount, often within a few business days. From that point forward, you'll make consistent monthly payments until the loan is fully repaid. This predictability is one of the key advantages of personal loans for budgeting and financial planning purposes.

Most personal loans are unsecured, meaning they don't require you to pledge assets like your home or car as collateral. This reduces your risk of losing property if you default, but it also means lenders charge higher interest rates compared to secured loans to compensate for their increased risk. Some lenders do offer secured personal loans with lower rates, but these require collateral and carry the risk of asset seizure in case of non-payment.

The versatility of personal loans is another defining characteristic. While some loan types restrict how you can use the funds, personal loans generally allow you to use the money for almost any legal purpose—from consolidating high-interest credit card debt to financing a wedding, covering medical expenses, or making home improvements. This flexibility, combined with fixed rates and predictable payments, makes personal loans a popular choice for consumers managing various financial needs.

The typical personal loan application process from initial research to receiving funds

Understanding Interest Rates and Repayment Terms

Interest rates on personal loans vary significantly based on multiple factors, with Annual Percentage Rates (APRs) typically ranging from 6% to 36%. Your specific rate depends primarily on your credit score, income level, debt-to-income ratio, and the lender's assessment of your overall financial stability. Borrowers with excellent credit scores (740 and above) often qualify for rates in the single digits, while those with fair or poor credit may face rates exceeding 20% or higher.

The APR is crucial because it represents the true cost of borrowing, incorporating not just the interest rate but also any fees charged by the lender, such as origination fees, processing fees, or prepayment penalties. When comparing loan offers, always focus on the APR rather than just the stated interest rate. A loan with a lower interest rate but high fees might actually cost more than one with a slightly higher rate but minimal fees.

Repayment terms directly impact your monthly payment amount and the total interest you'll pay over the life of the loan. Shorter loan terms (24-36 months) mean higher monthly payments but significantly less interest paid overall. Longer terms (60-84 months) reduce your monthly obligation but increase the total cost of the loan substantially. For example, a $10,000 loan at 10% APR paid over three years costs approximately $1,616 in interest, while the same loan over six years costs about $3,227—nearly double the interest for the extended term.

Most personal loans feature fixed interest rates, meaning your rate and monthly payment remain constant throughout the loan term. This predictability is valuable for budgeting and financial planning. However, some lenders offer variable-rate personal loans with rates tied to market indexes. While these might start with lower rates, they carry the risk of increasing over time, potentially making your loan more expensive and your payments less predictable. For most borrowers, the stability of fixed-rate loans outweighs the potential initial savings of variable rates.

Credit Score Requirements and Their Impact on Loan Terms

Your credit score is the single most influential factor in determining whether you'll be approved for a personal loan and what terms you'll receive. Credit scores range from 300 to 850, with most lenders categorizing scores as follows: poor (300-579), fair (580-669), good (670-739), very good (740-799), and excellent (800-850). While some lenders will work with borrowers who have fair or even poor credit, the best rates and terms are reserved for those with good to excellent credit.

The difference in interest rates across credit tiers can be dramatic and costly. A borrower with excellent credit might qualify for a personal loan at 7% APR, while someone with fair credit could face rates of 20% or higher for the same loan amount and term. On a $15,000 five-year loan, this difference translates to approximately $5,000 more in interest payments—a substantial premium for lower creditworthiness. This reality underscores the importance of building and maintaining strong credit as part of your overall financial literacy and money management strategy.

Before applying for a personal loan, it's wise to check your credit score and review your credit reports from all three major bureaus (Equifax, Experian, and TransUnion). Look for errors or inaccuracies that could be dragging down your score, and dispute any mistakes you find. Even small improvements to your credit score can result in better loan terms. If your score is lower than you'd like, consider taking a few months to improve it before applying—paying down existing debts, making all payments on time, and reducing credit utilization can boost your score relatively quickly.

For borrowers with limited or damaged credit, options still exist, though they come with trade-offs. Some lenders specialize in loans for fair or poor credit, but expect higher interest rates and potentially stricter terms. Alternatively, adding a creditworthy co-signer can help you qualify for better rates, though this places financial responsibility on both parties. Secured personal loans, which require collateral, may also offer more favorable terms for those with credit challenges, though they carry the risk of losing the pledged asset if you default.

When Personal Loans Make Financial Sense

Personal loans can be valuable financial tools in specific situations, but they're not always the best solution. Understanding when a personal loan makes sense versus when alternative options might be better is crucial for smart spending and effective financial planning. One of the most common and financially sound uses of personal loans is debt consolidation—combining multiple high-interest debts, particularly credit card balances, into a single loan with a lower interest rate and fixed repayment schedule.

Debt consolidation through a personal loan makes sense when you can secure an interest rate significantly lower than what you're currently paying on credit cards or other debts. For example, if you're carrying $20,000 in credit card debt at an average rate of 18%, consolidating with a personal loan at 10% could save you thousands in interest and help you become debt-free faster with structured payments. However, this strategy only works if you address the underlying spending habits that led to the debt in the first place—otherwise, you risk running up new credit card balances while still paying off the consolidation loan.

Personal loans also make sense for financing necessary expenses that will improve your financial situation or quality of life, such as home improvements that increase property value, medical procedures not covered by insurance, or educational expenses that enhance earning potential. The key is ensuring the expense is truly necessary and that the loan terms are favorable enough that the benefit outweighs the cost of borrowing. For discretionary expenses like vacations or luxury purchases, personal loans are generally not advisable—these should be saved for rather than financed.

Emergency situations sometimes necessitate personal loans when you lack sufficient emergency savings. While building an emergency fund should be a priority in your budgeting tips and savings strategies, unexpected medical bills, urgent home repairs, or sudden job loss can create immediate financial needs. In these cases, a personal loan may be preferable to high-interest credit cards or predatory payday loans. However, this underscores the importance of establishing emergency savings as part of your wealth building strategy to avoid relying on borrowed money for unexpected expenses.

Common Pitfalls to Avoid When Taking Personal Loans

One of the most significant mistakes borrowers make is failing to shop around and compare offers from multiple lenders. Interest rates, fees, and terms can vary dramatically between lenders, and accepting the first offer you receive could cost you thousands of dollars over the life of the loan. Take time to get quotes from at least three to five lenders, including traditional banks, credit unions, and reputable online lenders. Many lenders offer pre-qualification with soft credit checks that won't impact your credit score, allowing you to compare rates without penalty.

Another common pitfall is borrowing more than you actually need. Lenders often approve borrowers for larger amounts than requested, and it's tempting to take the maximum available. However, every dollar borrowed costs money in interest, and larger loans mean larger monthly payments that strain your budget. Carefully calculate the exact amount you need and resist the urge to borrow extra "just in case." This discipline is essential for maintaining financial freedom and avoiding the debt trap that ensnares many borrowers.

Ignoring fees and focusing solely on interest rates is another costly mistake. Origination fees, which typically range from 1% to 8% of the loan amount, are often deducted from your loan proceeds, meaning you receive less than you borrowed but pay interest on the full amount. Late payment fees, prepayment penalties, and other charges can add up quickly. Always review the complete fee structure and calculate the total cost of the loan, not just the monthly payment. Some loans with slightly higher interest rates but no fees may actually be less expensive overall than loans with lower rates but substantial fees.

Finally, many borrowers underestimate the importance of reading and understanding the loan agreement before signing. Loan contracts contain crucial information about your rights and obligations, including what happens if you miss payments, whether you can pay off the loan early without penalty, and what recourse the lender has if you default. Taking time to read the fine print and asking questions about anything unclear can prevent unpleasant surprises down the road. If a lender pressures you to sign quickly without allowing time to review the terms, consider it a red flag and look elsewhere for financing.

Practical Checklist for Evaluating Personal Loan Offers

Before accepting any personal loan offer, use this comprehensive checklist to ensure you're making an informed decision that aligns with your financial goals and money management principles. This systematic approach helps you compare offers objectively and identify the best option for your specific situation.

Interest Rate and APR Comparison

- What is the stated interest rate, and is it fixed or variable?

- What is the APR, which includes all fees and represents the true cost of borrowing?

- How does this APR compare to other offers you've received?

- If the rate is variable, what index is it tied to, and what are the rate caps?

Fees and Additional Costs

- Is there an origination fee, and if so, what percentage of the loan amount?

- Are there application fees, processing fees, or other upfront costs?

- What is the late payment fee, and when is it assessed?

- Is there a prepayment penalty if you pay off the loan early?

- Are there any annual fees or maintenance charges?

Loan Terms and Repayment

- What is the loan term (repayment period), and can you afford the monthly payment?

- What is the total amount you'll repay over the life of the loan (principal plus interest)?

- When is the first payment due, and what is the payment schedule?

- Does the lender offer flexible payment options or hardship programs if needed?

- Can you make extra payments or pay off the loan early without penalty?

Lender Reputation and Service

- Is the lender reputable with positive customer reviews and ratings?

- How quickly will you receive the funds after approval?

- What customer service options are available (phone, email, chat)?

- Does the lender report to credit bureaus (important for building credit)?

- Are there any complaints or red flags about the lender's practices?

Personal Financial Assessment

- Does this loan fit within your monthly budget without causing financial strain?

- Have you calculated your debt-to-income ratio with this new loan included?

- Do you have a clear plan for using the loan proceeds responsibly?

- Have you considered alternatives like using savings or a lower-cost option?

- Will this loan help you achieve your financial goals or create new problems?

Working through this checklist systematically ensures you don't overlook important details that could affect your financial well-being. Take your time, compare multiple offers side by side, and don't hesitate to ask lenders questions about anything that's unclear. Remember that taking on debt is a serious financial commitment that will impact your budget and financial freedom for years to come, so thorough evaluation is essential for making the right choice.

Making Informed Borrowing Decisions

Personal loans can be powerful tools for achieving financial goals, consolidating debt, or managing unexpected expenses when used wisely and with full understanding of their costs and implications. The key to successful borrowing lies in thorough research, honest assessment of your financial situation, and careful comparison of loan offers to find terms that truly serve your best interests. By understanding how interest rates work, recognizing the impact of your credit score, and avoiding common pitfalls, you position yourself to make borrowing decisions that support rather than undermine your long-term financial health.

Remember that the best loan is often the one you don't need to take because you've built sufficient emergency savings and practiced disciplined money management. However, when borrowing becomes necessary or strategically advantageous, approaching the process with knowledge and caution ensures you get the best possible terms and avoid the debt traps that plague many borrowers. Use the checklist provided, take your time comparing offers, and never feel pressured to accept terms that don't feel right or that you don't fully understand.

Financial literacy and informed decision-making are your greatest assets in navigating the world of personal finance. Whether you're considering your first personal loan or refinancing existing debt, the principles outlined in this guide—understanding true costs, evaluating your creditworthiness, recognizing when loans make sense, and avoiding common mistakes—will serve you well. By applying these insights and maintaining a commitment to responsible borrowing and smart spending, you can use personal loans as tools for financial progress rather than sources of financial stress.

About the Author

This article was prepared by the Financial Education Hub editorial team, dedicated to providing accurate, unbiased information about personal finance topics. Our content is thoroughly researched and designed to help readers make informed financial decisions. We do not provide personalized financial advice and recommend consulting with qualified financial professionals for individual guidance.